- 1 What inflation actually does to your salary

- 2 Nominal vs real salary: the difference most people overlook

- 3 Infographic: Inflation & Salary: Why Your Income Feels Smaller

- 4 How inflation impacts different income levels

- 5 Where people feel inflation the most

- 6 Typical mistakes people make when dealing with inflation

- 7 How to adapt your salary strategy to inflation

- 8 Real-life scenario: how inflation changes financial behavior

-

9

FAQ: common questions about inflation and salary

- 9.1 Does a salary raise always protect against inflation?

- 9.2 Why does inflation feel stronger than official numbers?

- 9.3 Can changing jobs help offset inflation?

- 9.4 Is saving money still effective during inflation?

- 9.5 How often should salary be adjusted?

- 9.6 Does inflation affect remote workers differently?

- 10 Short version: what to do right now

- 11 Conclusion: the key shift in thinking

- 12 Sources

Have you ever received a raise… and still felt like you’re not moving forward financially?

Your salary increased. On paper, everything looks fine. But your grocery bill is higher. Rent eats up more of your income. Even small everyday purchases feel heavier. It creates a strange contradiction: you earn more, but it feels like less.

This is exactly how inflation works. It doesn’t just affect prices — it quietly reshapes the real value of your income.

What inflation actually does to your salary

Inflation is often explained as “prices going up.” That’s technically correct, but incomplete. The more important part is this:

Inflation reduces the purchasing power of your salary.

In simple terms, your money buys less than it used to.

Imagine this:

- Last year: $1,000 covered rent, food, and some savings

- This year: the same $1,000 barely covers rent and basic groceries

Your salary didn’t change. But its real value did.

“Inflation is taxation without legislation.” — Milton Friedman

This quote highlights a key idea: inflation acts like a silent cost, gradually eroding your financial stability.

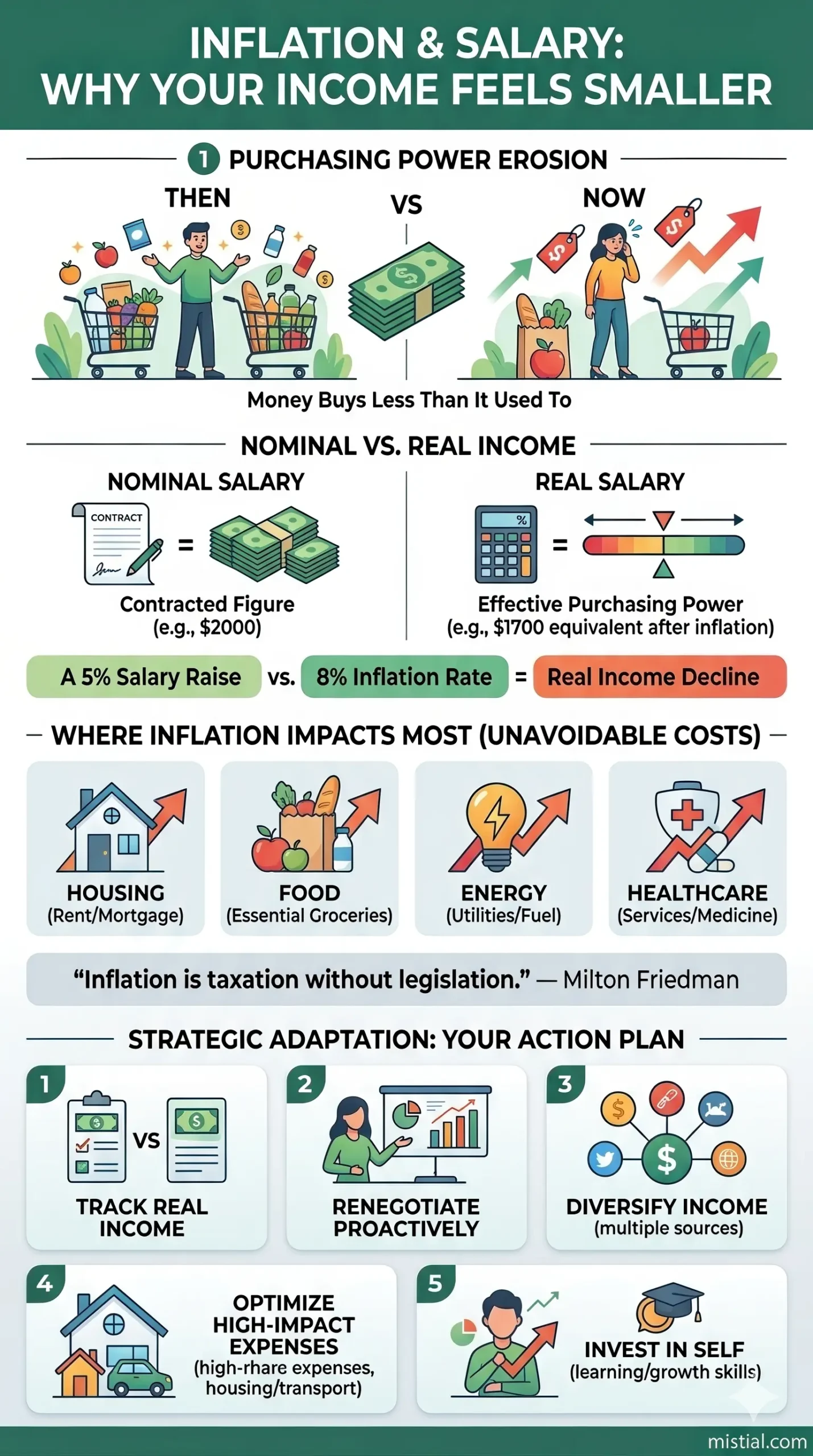

Nominal vs real salary: the difference most people overlook

To understand the impact properly, you need to distinguish between two concepts:

| Type | What it means | Example |

|---|---|---|

| Nominal salary | The number you see in your contract | $2,000/month |

| Real salary | What your money can actually buy | Equivalent of $1,700 after inflation |

A salary increase doesn’t automatically mean you’re better off.

If your salary grows by 5%, but inflation is 8%, you’re effectively losing purchasing power.

Why this matters in everyday life

This is where people start noticing subtle changes:

- You delay purchases you previously made without thinking

- You switch to cheaper alternatives more often

- Savings become harder to maintain

- Unexpected expenses feel more stressful

It’s not always dramatic. Often, it’s gradual — and that’s why it’s easy to underestimate.

Infographic: Inflation & Salary: Why Your Income Feels Smaller

How inflation impacts different income levels

Inflation doesn’t affect everyone equally. Its impact depends on how your income is structured.

1. Fixed salary employees

If your income is stable but not regularly adjusted, inflation hits directly.

Example: An employee earning the same salary for two years in a high-inflation environment experiences a real income decline without any visible salary change.

2. Freelancers and variable income workers

There is more flexibility, but also more pressure:

- You need to adjust pricing more frequently

- Clients may resist higher rates

- Income becomes less predictable

Inflation becomes a negotiation problem, not just an economic one.

3. High-income earners

They are less sensitive to basic price increases but still affected through:

- Investment performance

- Lifestyle inflation

- Long-term purchasing power erosion

Inflation affects everyone — just in different ways.

Where people feel inflation the most

Not all expenses rise equally. Some categories hit harder because they are unavoidable:

- Housing — rent or mortgage adjustments

- Food — frequent purchases amplify price changes

- Energy — utilities and fuel costs

- Healthcare — often increases faster than general inflation

These are not optional. That’s why even moderate inflation feels significant.

Typical mistakes people make when dealing with inflation

Many people react to inflation — but not always effectively.

1. Ignoring it completely

“Prices are just a bit higher” — this mindset leads to passive income loss over time.

2. Relying only on salary increases

Raises often lag behind inflation. Waiting for your employer to compensate fully may not work.

3. Cutting only “small” expenses

Reducing coffee or subscriptions helps, but major expenses (housing, transport) have a bigger impact.

4. Keeping all savings in cash

Cash loses value during inflation. Without any form of growth, your savings shrink in real terms.

5. Avoiding financial adjustments

Not reviewing your budget or income strategy means inflation continues to erode your finances unnoticed.

How to adapt your salary strategy to inflation

You can’t control inflation, but you can adjust your approach to income and spending.

1. Track your real income

Instead of focusing only on your salary number, ask:

What can I actually afford compared to last year?

2. Renegotiate income proactively

Whether you’re employed or freelance:

- Bring data (market rates, inflation trends)

- Show your value clearly

- Time discussions strategically (reviews, project milestones)

3. Diversify income sources

Relying on a single income stream increases vulnerability.

Even small additional sources can offset inflation pressure.

4. Focus on high-impact expenses

Instead of cutting everything:

- Review housing costs

- Optimize recurring payments

- Evaluate transportation expenses

These changes often matter more than minor savings.

5. Think in long-term value

Skills, education, and adaptability often protect income better than short-term adjustments.

“The best investment you can make is in yourself.” — Warren Buffett

Real-life scenario: how inflation changes financial behavior

Consider this situation:

Anna earns more than she did two years ago. But:

- Her rent increased by 25%

- Groceries cost noticeably more each month

- She saves less despite earning more

She didn’t become worse at managing money.

The environment changed.

This is a key shift: understanding that inflation is not a personal failure — it’s a structural factor that requires adaptation.

FAQ: common questions about inflation and salary

Does a salary raise always protect against inflation?

Not necessarily. It depends on whether the raise matches or exceeds inflation. Otherwise, real income may still decline.

Why does inflation feel stronger than official numbers?

Because personal expenses differ. Essential categories like food and housing often rise faster than average inflation rates.

Can changing jobs help offset inflation?

Sometimes. New positions may offer higher pay, but it depends on market conditions and your skills.

Is saving money still effective during inflation?

Yes, but how you save matters. Pure cash savings may lose value over time without any form of growth.

How often should salary be adjusted?

There’s no universal rule. In higher inflation environments, more frequent reviews may be necessary.

Does inflation affect remote workers differently?

It can. Especially if income is tied to one country while living costs rise in another.

Short version: what to do right now

- Review your real purchasing power, not just your salary number

- Start a conversation about income adjustment if needed

- Identify 1–2 major expenses you can optimize

- Explore at least one additional income source

- Invest in skills that increase your earning potential

Conclusion: the key shift in thinking

Inflation is not just an economic term. It’s something you feel in everyday decisions.

The key is not to react emotionally — but to adapt strategically.

Your salary is not just a number. It’s a dynamic value shaped by the environment.

Once you start thinking in real terms, your financial decisions become clearer and more effective.

Sources

- International Monetary Fund (IMF) — Inflation and Purchasing Power

- World Bank — Global Economic Prospects Reports

- OECD — Wage Growth and Inflation Analysis

- Milton Friedman — Monetary Theory and Policy

- Federal Reserve — Inflation and Household Economics

- Warren Buffett — Letters to Shareholders